How much house can you afford with the higher rates?

The housing market is beginning to slow as rates are on the rise. If you are in the market to purchase it is important to re-assess the affordability of your next home so that you will not feel house poor. As a general guideline the bank will approve you on a mortgage loan if your debt-to-income ratio doesn’t exceed 43%. Your debt to income compares your monthly debt payments to your monthly gross income. For example if you make $100K a year your monthly income is $8333. This means you could possibly get qualified for a loan payment(including your mortgage and escrow payment and other monthly debt obligations) of $3583 monthly. That $3583 monthly went much farther last year at this time with interest rates being in the 3s.

This fact has put pressure on the housing market for prices to come down as affordability is decreasing. What has primarily kept the housing market prices afloat has been inventory. The chart below shows the number of single family homes and condo units available for sale in the US(in thousands). As you can see inventory peaked when the housing market crashed during the great recession in 2007-2009. That inventory has steadily declined over time and it bottomed out during the beginning of COVID.

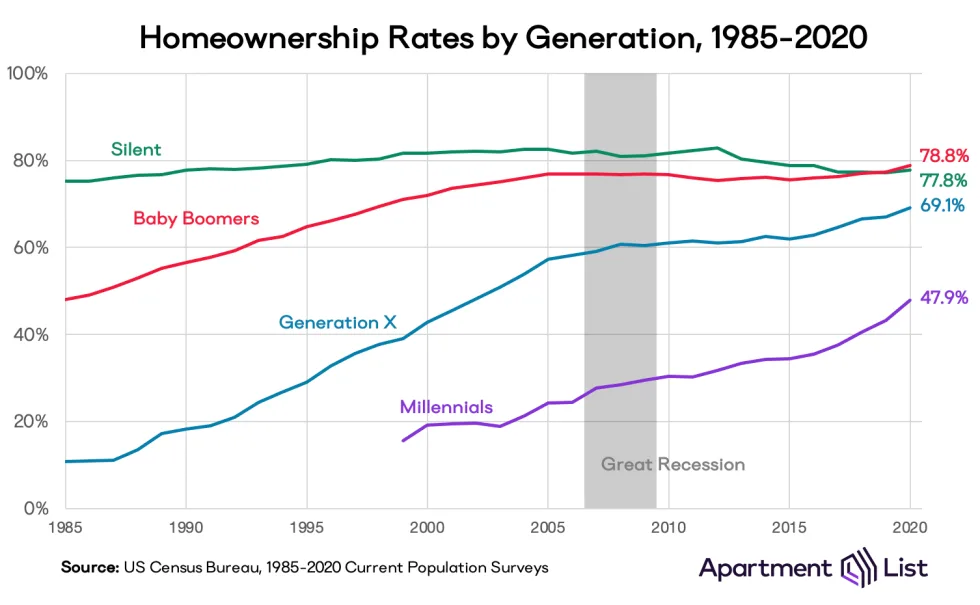

We don’t have a crystal ball but this lack of inventory will probably prevent the housing market from “crashing” as the demand far outweighs the supply. It does result however in many having to make tough decisions regarding how much house they want to afford. This pressure is specifically felt by millennials, of which the majority, do not own homes. As the millennial generation ages more of them will be looking to purchase in the next 5-10 years.

When it comes to how much house you want to afford you want to look at the % of income your total house payment would be. Seeing that most people aren’t buying houses cash that debt payment from the mortgage will encompass their biggest monthly expense. Ideally your total debt outlay(including cars, student loans, etc) would not exceed 30%. I say ideally, from the perspective the size of your house payment doesn’t significantly impact your ability to save or spend on many of the discretionary items you probably are currently accustomed to. In my experience if you are determined to retire early(as a normal W-2 worker) your house expense you would want to keep it around 20%. If you plan to work towards a more traditional retirement age then going closer to that 30% is okay. You can see below the housing cost a sample married couple would be assessing today based on the rate changes.

Example - $200K income married couple

The good old days at 3.5% rates

Ideal housing budget for FI(financial independence) - $525K (5% DP)

Ideal budget if you carry other debt - $650K(5% DP)

Max - $790K(5% DP)

Current great rate today at 6.5%

Ideal housing budget for FI - $400K (5% DP)

Ideal budget if you carry with other debt - $515K(5% DP)

Max - $615K(5% DP)

However life is all about choices so here are some suggestions if you are looking to buy a house that costs more than 30% of your monthly income.

Tips

- Look at creating a side hustle for extra income

- Clearly increasing the income part of the equation would lower the overall % your housing cost makes up.

- House hack

- If you can stomach it and are creative you could purchase a property that could accommodate a roommate or has a separate dwelling unit. This rental income would reduce your overall housing cost.

- Resolve to work longer or downsize sooner

- If you are intent on purchasing a house at the top of what the bank will qualify you for then you may be forced to work longer to get to your long term financial goals. Also you may decide to only live in the house during your child raising years and then downsize.

- Reduce discretionary spending

- You generally want to leave enough room in your budget that would allow you to save at least 15%. This means for a married couple making $200K( roughly 20% of their income would be going to taxes) would have 65% to spend on housing plus discretionary spending. If you decide to put more into your house that would leave less toward the discretionary percentage without sacrificing your savings.